Portfolio down 2.1% in the year. A very volatile year. Up strongly in Q1, fell back even more strongly in Q2. Broadly even in Q3 and the Q4 fall was very much a December affair.

CAGR since inception (March 2016) down to 13.5%.

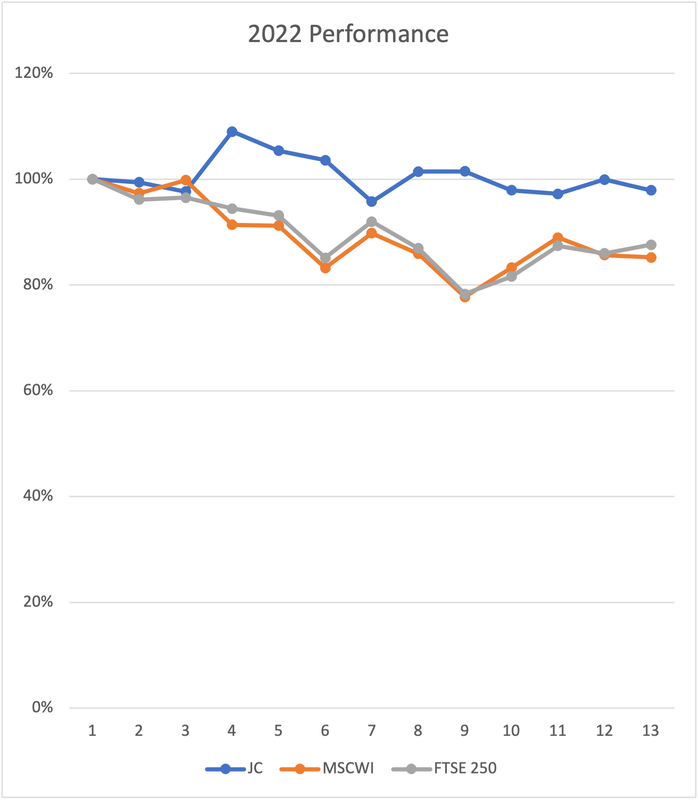

Comparing returns to the MSCI World Index and FTSE 250 I get the following return profile. It is only one year but the first one since 2016 that has been negative.

CAGR since inception (March 2016) down to 13.5%.

Comparing returns to the MSCI World Index and FTSE 250 I get the following return profile. It is only one year but the first one since 2016 that has been negative.

Whilst pain has been widespread across the portfolio the two big problems have been;

(a) US tech. I hold larger positions in GOOGL, AAAPL, MSFT and META and they have all suffered.

(b) MPAC the packaging business that I had a significant (to my portfolio) position in. They had a so so pandemic, and then a poor return. I would agree with their decision to prioritise meeting customer needs but this came at a high operating cost. The CEO is IMHO opinion good, but the rest of the senior team is still open to consideration.

Of course there are never only 2 problems, but those were the biggest. That being said my other “with hindsight” appraisal would be to consider who you are getting into bed with. There are three small investments that I made this year on a value basis where over time I am facing that fact that I may be able to buy a £1 for 10p, but I am not sure management will not turn that £1 into 90p in their pocket. However I am less sure that these are genuine mistakes as with a deep value investment, and these were all deep value, you have to accept that you are going to kiss a lot of frogs. Schloss was often prepared to buy quickly and repent slowly.

On the plus side I have had 3 blockbusters.

(a) Pilbara Minerals who mine Lithium in Australia. V much off their highs for the year but still up 30%.

(b) Crocs the shoemaker. The company has been doing well for a while but took on a lot of debt to buy another footwear brand “Hey Dude”. Market hated the debt they took on and a buying opportunity arose. After a number of buys I am up about 55%.

(c) Thungela the coal company. Divested by Anglo American it went from a company whose owner did not want it and senior management were avoiding to one where the leadership were focused on coal. Lots of easy wins taken and on top of that a resurgent coal price as the non western world, in particular China, goes very heavily into coal as their transition energy. I have made a few buys but even with rising prices have doubled my money. Also the dividend was so large that I have had about 50% of my initial cost base returned.

I have reviewed all my holdings and whilst there are a number I have changed the target price on there are currently none that I am looking to sell. Though that is caveated by the approaching tax year end and the ability to harvest tax losses. At that point the rebuy or allocate elsewhere question is very apparent.

This year I read Richer, Wiser, Happier by William Green which is I think a truly excellent book for anyone interested in investing. I need to read it again and I will be trying to incorporate some of the lessons in it into my own investing. Of all the books on investing, and I have read quite a few, this is IMHO, one of the two best. The other is The Manual of Ideas by John Mihaljevic but that is very much a Value Investors book so if you are not a value investor perhaps less useful.

So whilst going forward my approach will remain directed towards traditional Value metrics. (Though I do think that I will be trying to refine my approach towards companies with Thomas Russo’s “capacity to suffer”). I am looking more at larger, longer term compounders to do the lifting over years rather than months.

(a) US tech. I hold larger positions in GOOGL, AAAPL, MSFT and META and they have all suffered.

(b) MPAC the packaging business that I had a significant (to my portfolio) position in. They had a so so pandemic, and then a poor return. I would agree with their decision to prioritise meeting customer needs but this came at a high operating cost. The CEO is IMHO opinion good, but the rest of the senior team is still open to consideration.

Of course there are never only 2 problems, but those were the biggest. That being said my other “with hindsight” appraisal would be to consider who you are getting into bed with. There are three small investments that I made this year on a value basis where over time I am facing that fact that I may be able to buy a £1 for 10p, but I am not sure management will not turn that £1 into 90p in their pocket. However I am less sure that these are genuine mistakes as with a deep value investment, and these were all deep value, you have to accept that you are going to kiss a lot of frogs. Schloss was often prepared to buy quickly and repent slowly.

On the plus side I have had 3 blockbusters.

(a) Pilbara Minerals who mine Lithium in Australia. V much off their highs for the year but still up 30%.

(b) Crocs the shoemaker. The company has been doing well for a while but took on a lot of debt to buy another footwear brand “Hey Dude”. Market hated the debt they took on and a buying opportunity arose. After a number of buys I am up about 55%.

(c) Thungela the coal company. Divested by Anglo American it went from a company whose owner did not want it and senior management were avoiding to one where the leadership were focused on coal. Lots of easy wins taken and on top of that a resurgent coal price as the non western world, in particular China, goes very heavily into coal as their transition energy. I have made a few buys but even with rising prices have doubled my money. Also the dividend was so large that I have had about 50% of my initial cost base returned.

I have reviewed all my holdings and whilst there are a number I have changed the target price on there are currently none that I am looking to sell. Though that is caveated by the approaching tax year end and the ability to harvest tax losses. At that point the rebuy or allocate elsewhere question is very apparent.

This year I read Richer, Wiser, Happier by William Green which is I think a truly excellent book for anyone interested in investing. I need to read it again and I will be trying to incorporate some of the lessons in it into my own investing. Of all the books on investing, and I have read quite a few, this is IMHO, one of the two best. The other is The Manual of Ideas by John Mihaljevic but that is very much a Value Investors book so if you are not a value investor perhaps less useful.

So whilst going forward my approach will remain directed towards traditional Value metrics. (Though I do think that I will be trying to refine my approach towards companies with Thomas Russo’s “capacity to suffer”). I am looking more at larger, longer term compounders to do the lifting over years rather than months.

RSS Feed

RSS Feed